Research system

ETF Portfolio Research

A reproducible pipeline that optimizes an ETF portfolio, walk-forward backtests it against benchmarks, and renders the whole result as an interactive report — open it below and inspect every assumption for yourself.

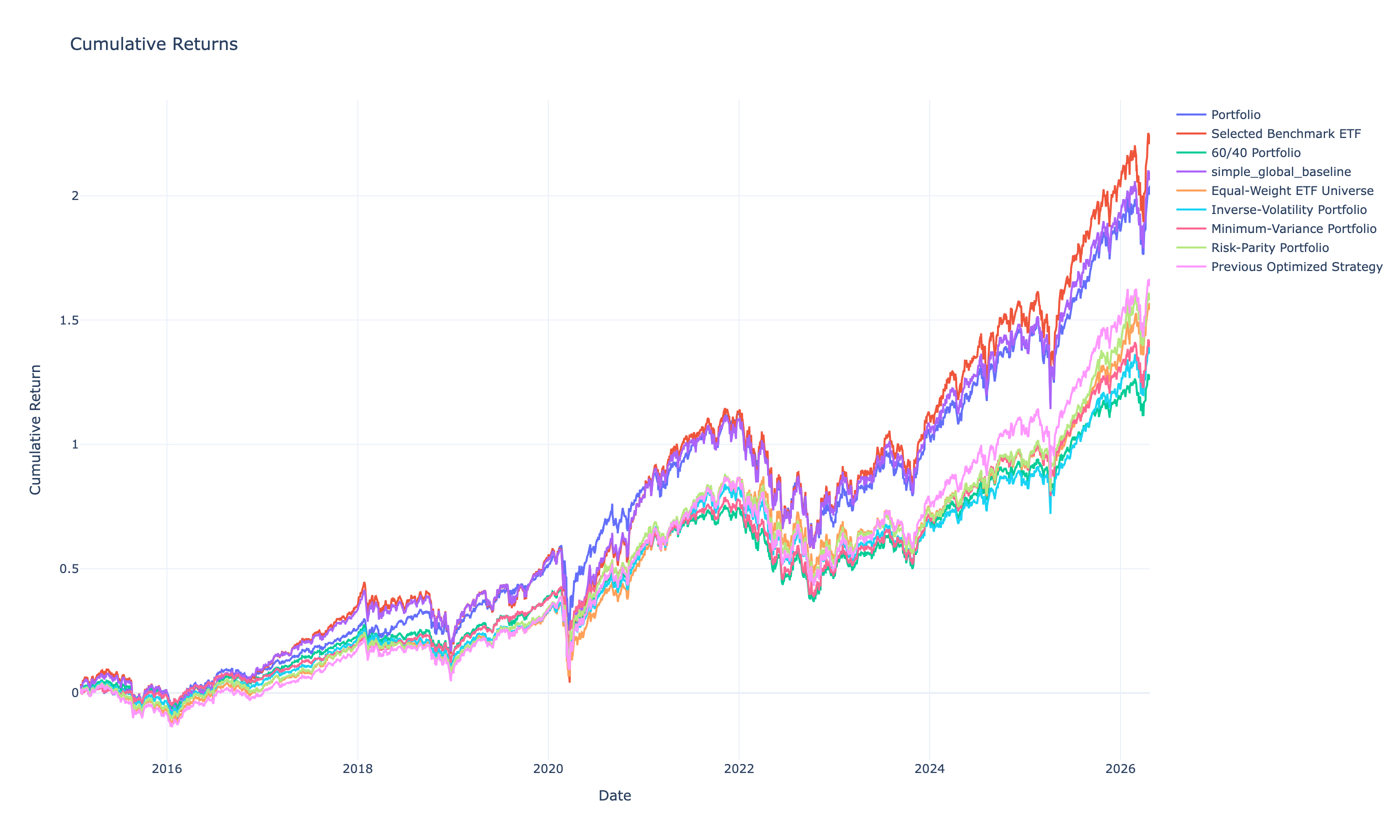

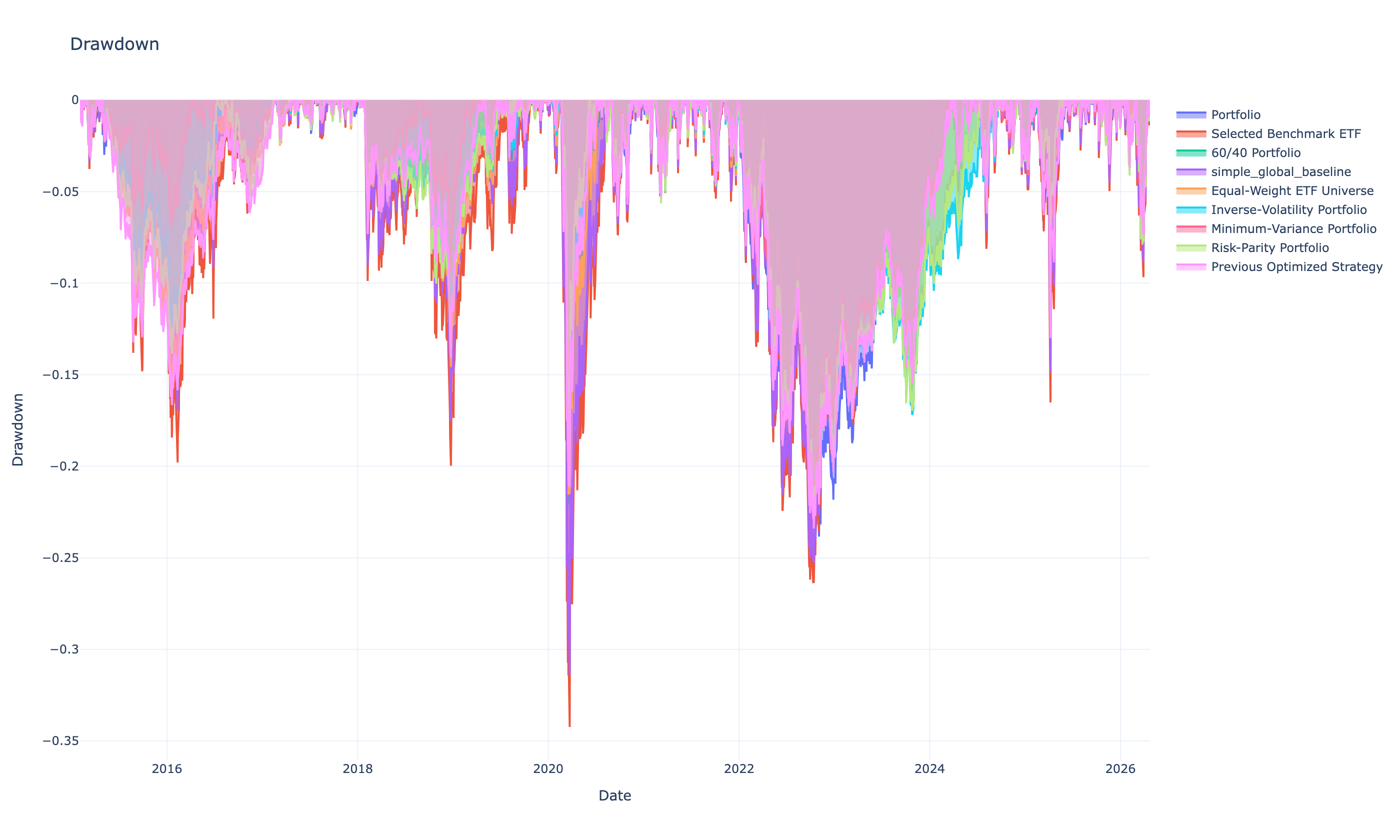

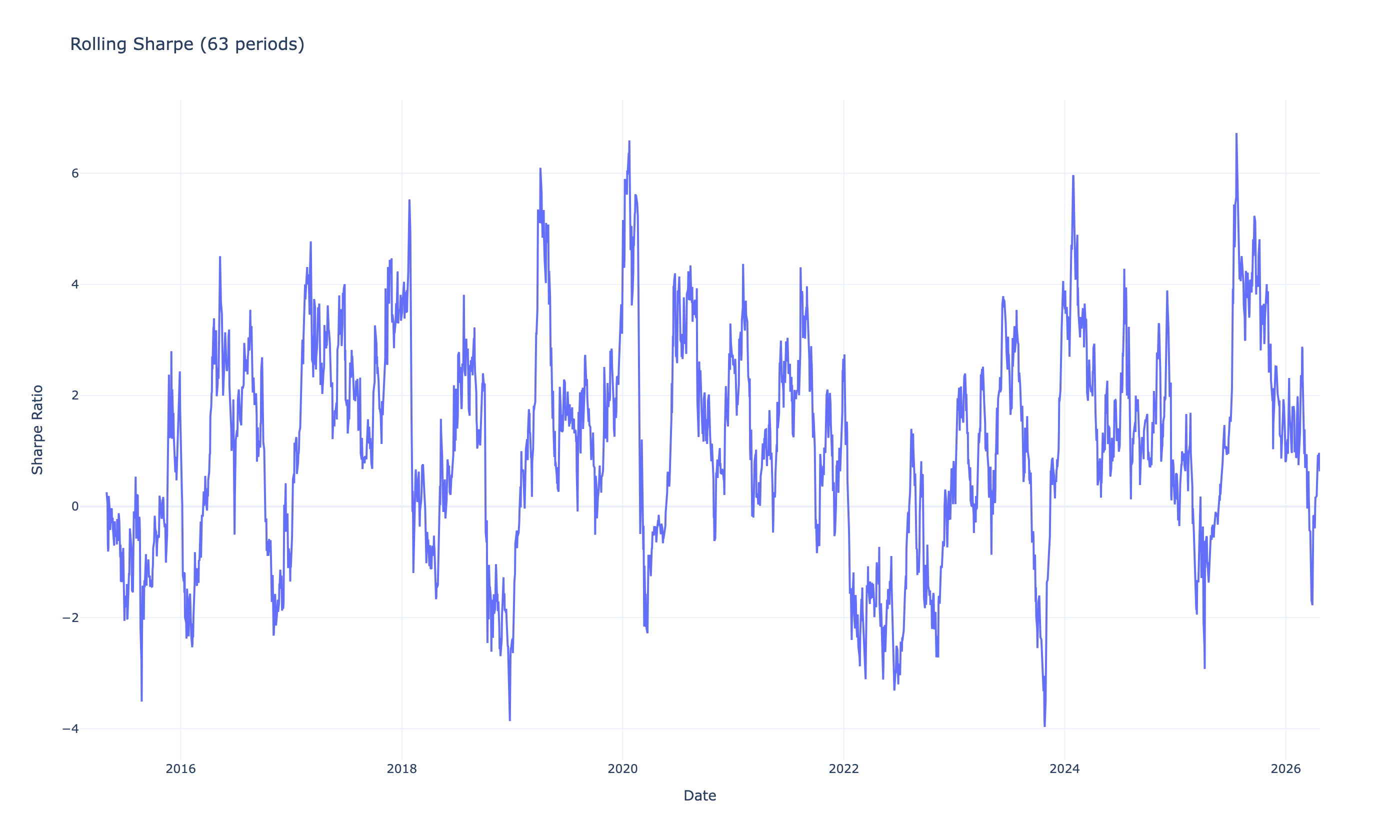

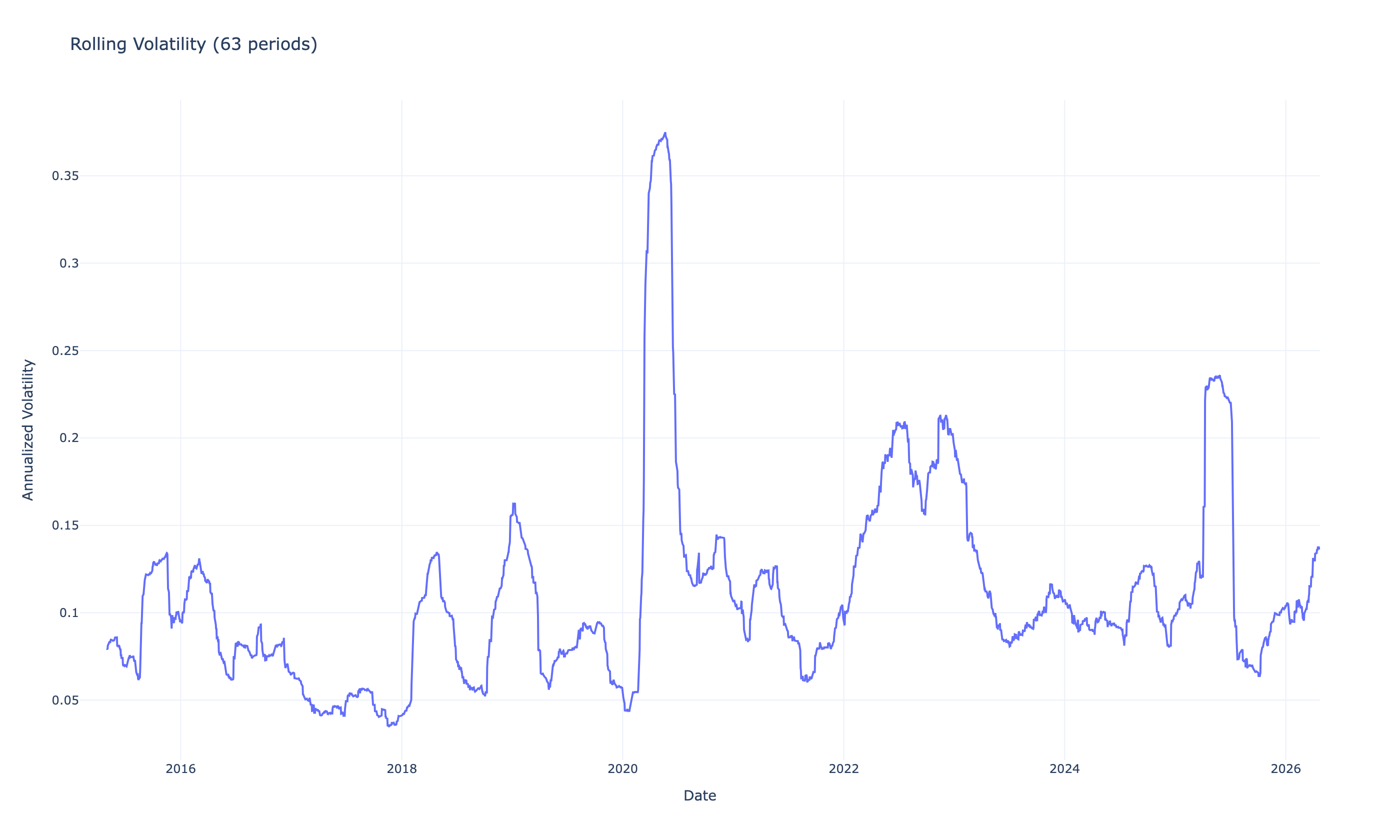

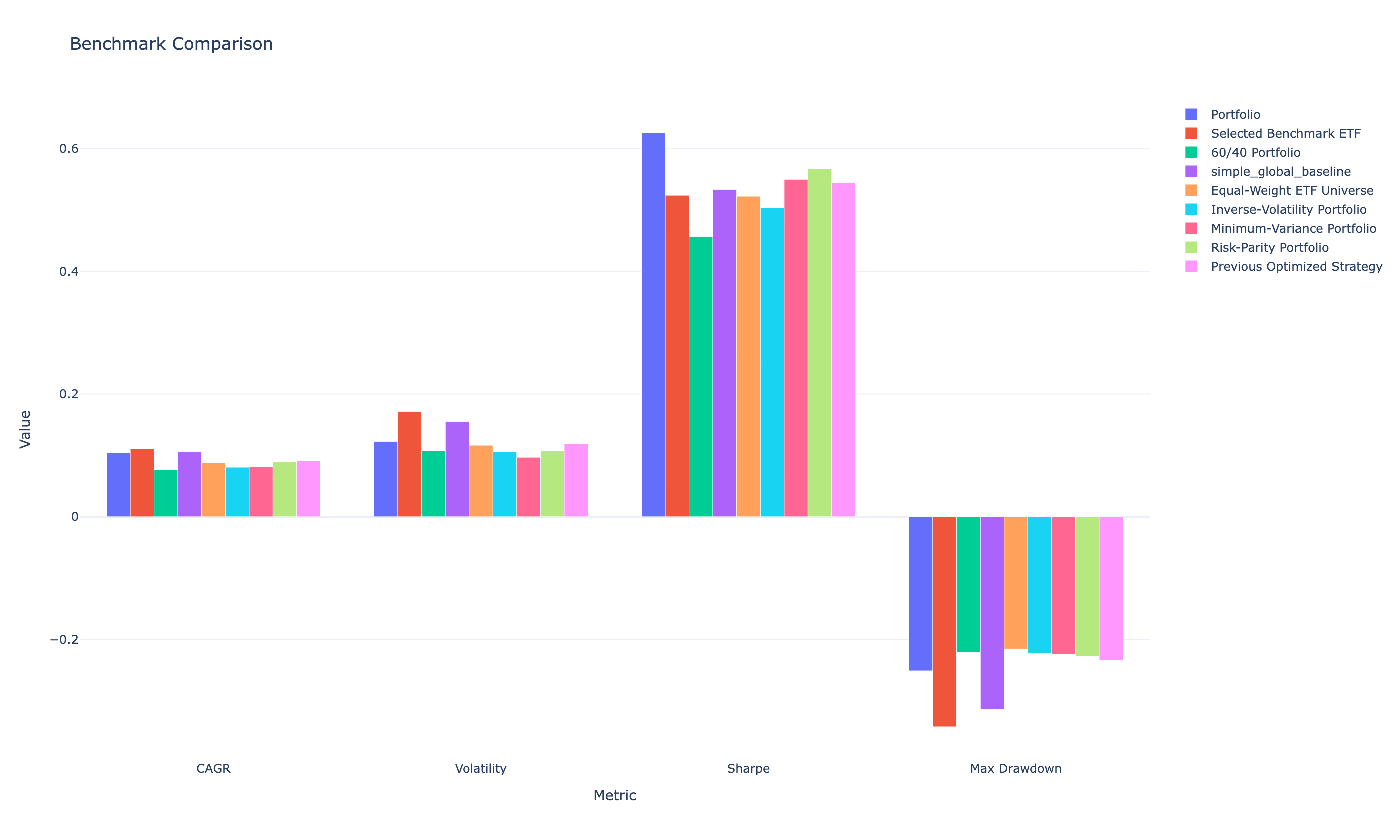

Performance

Strategy vs. benchmarks.

| Portfolio | CAGR | Sharpe | Sortino | Max DD | Volatility | Alpha | Beta | Calmar |

|---|---|---|---|---|---|---|---|---|

| Loading metrics… | — | — | — | — | — | — | — | — |

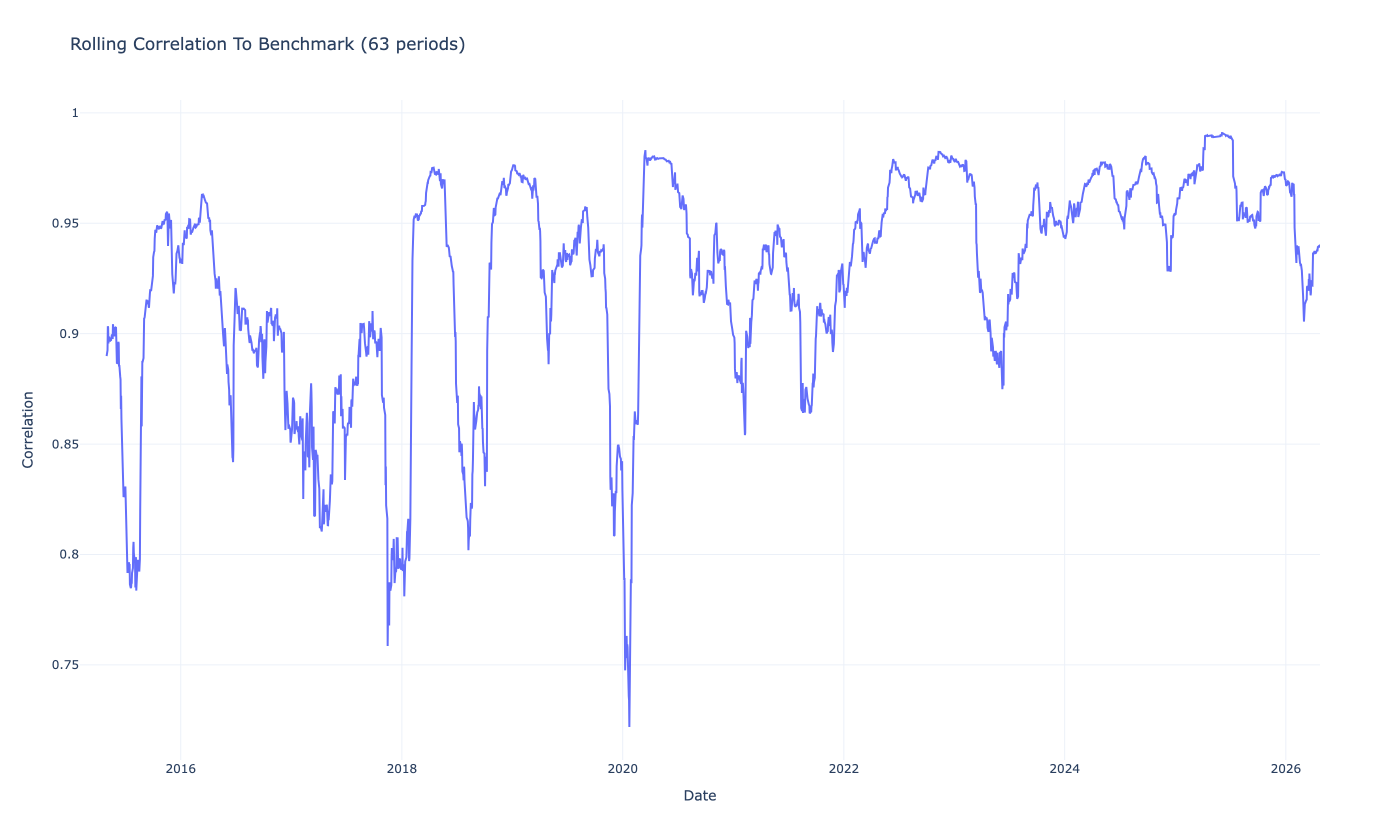

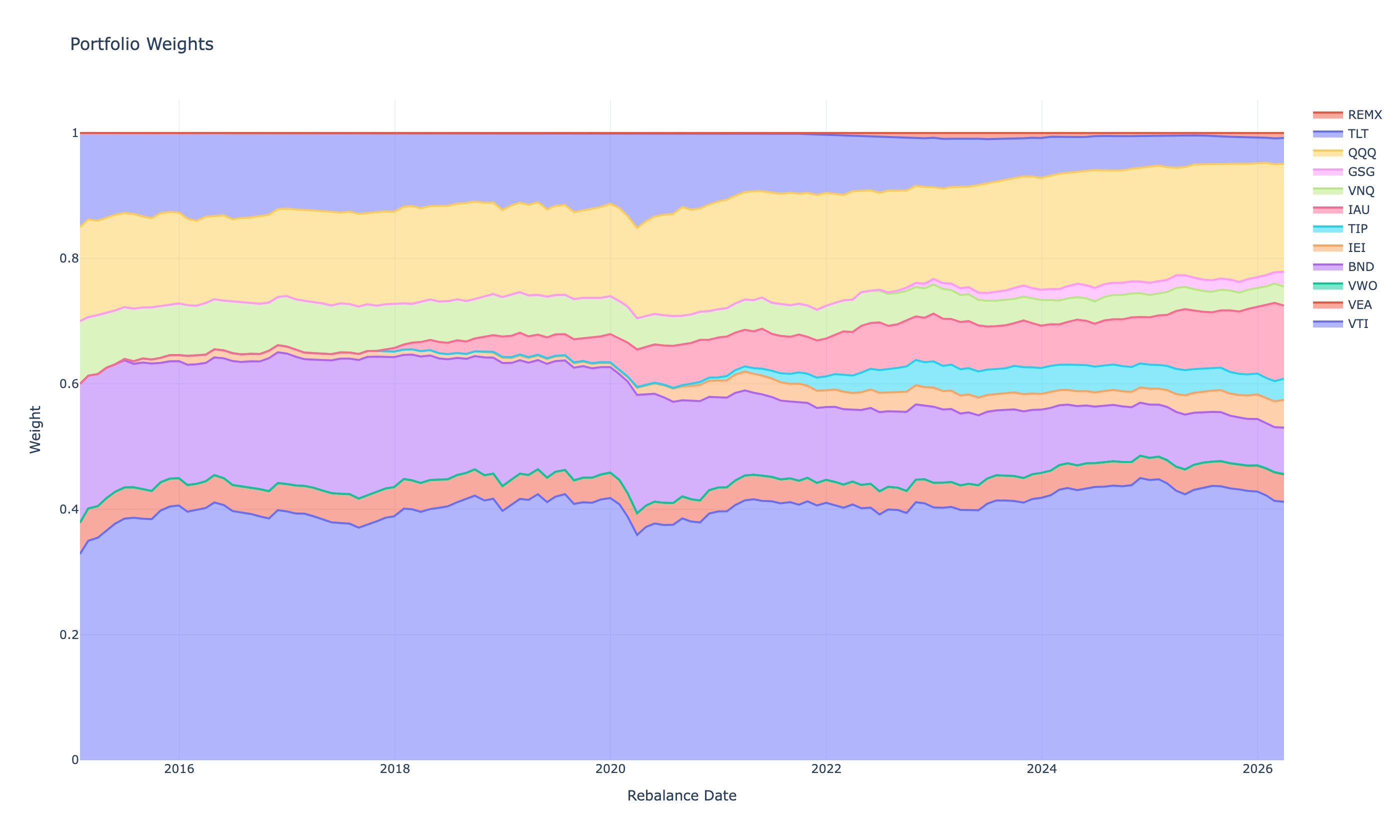

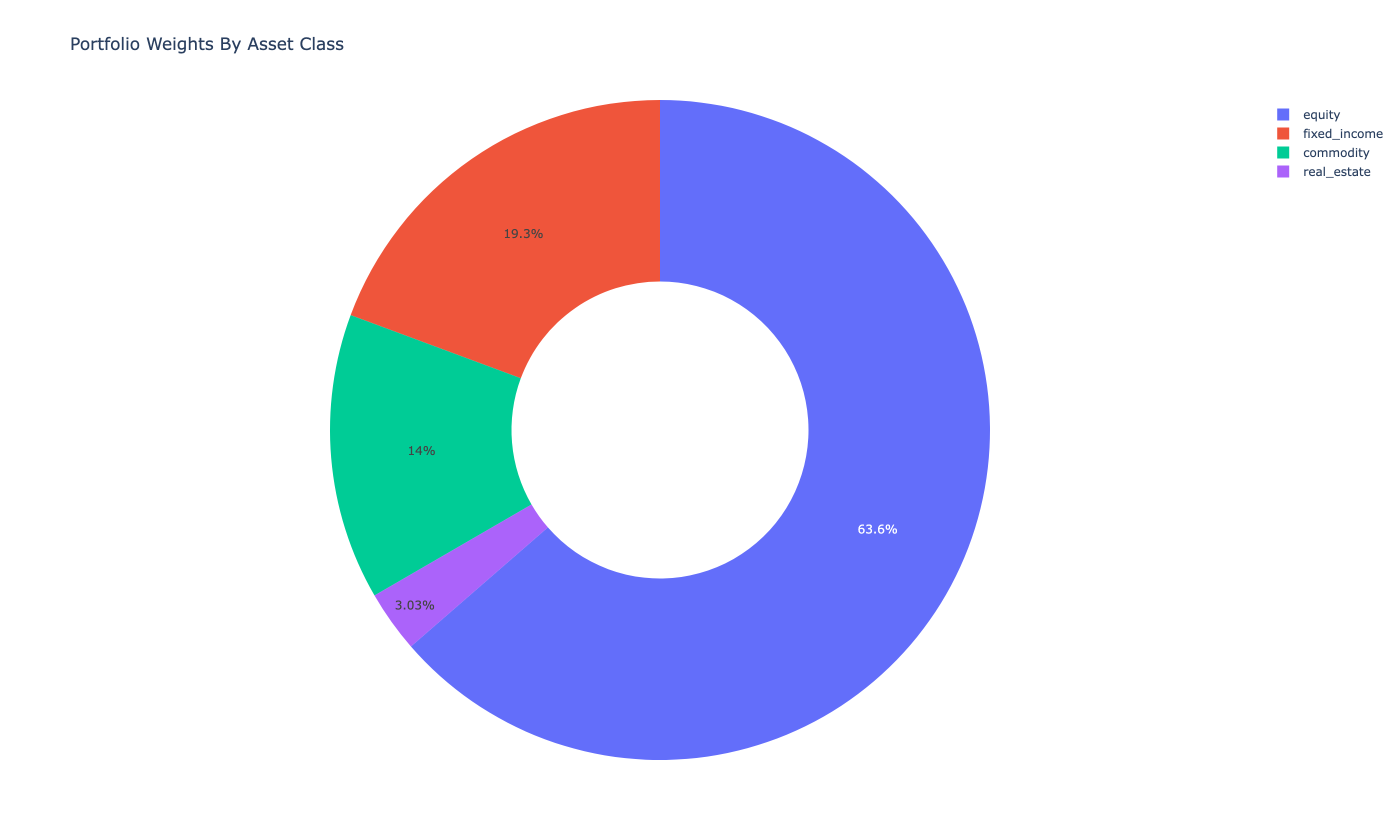

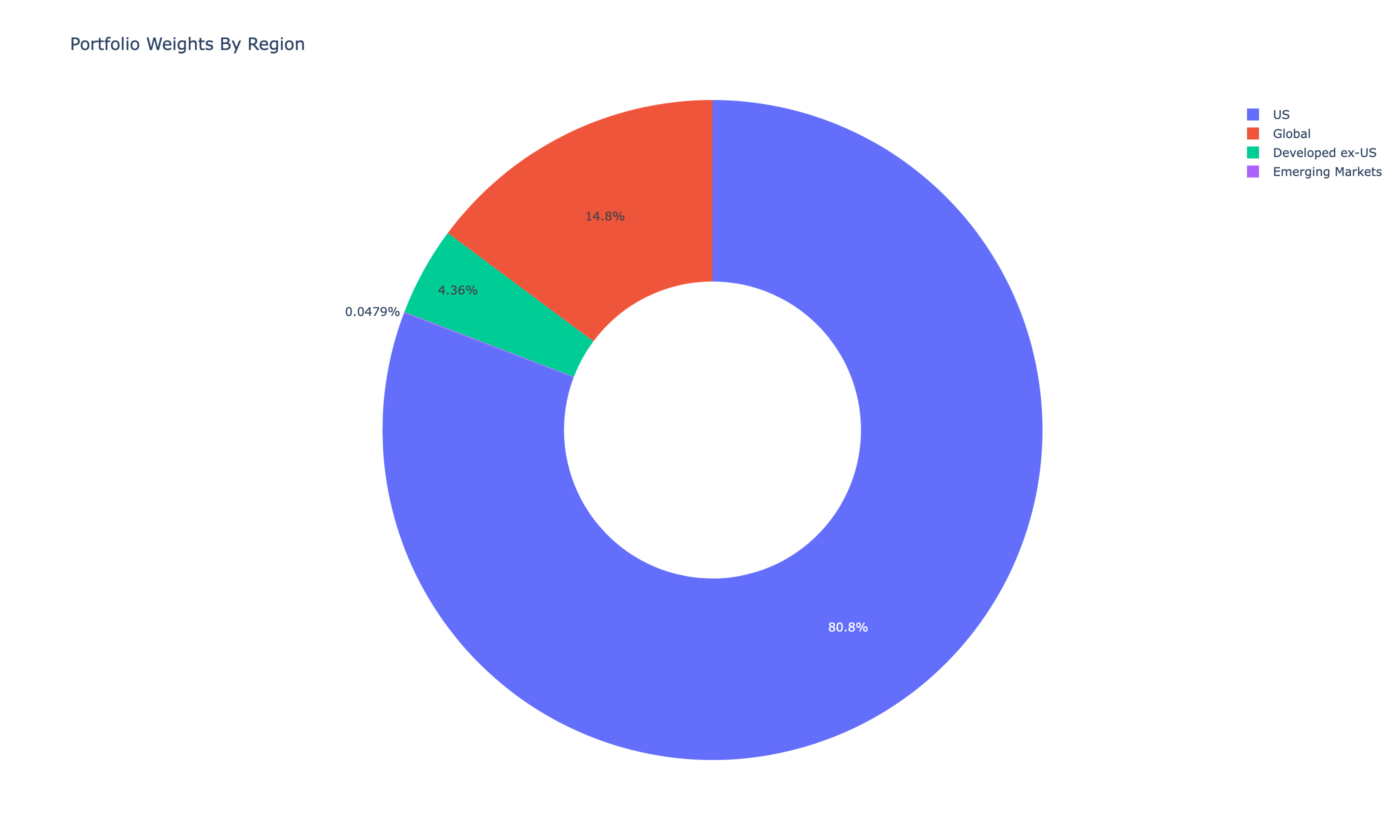

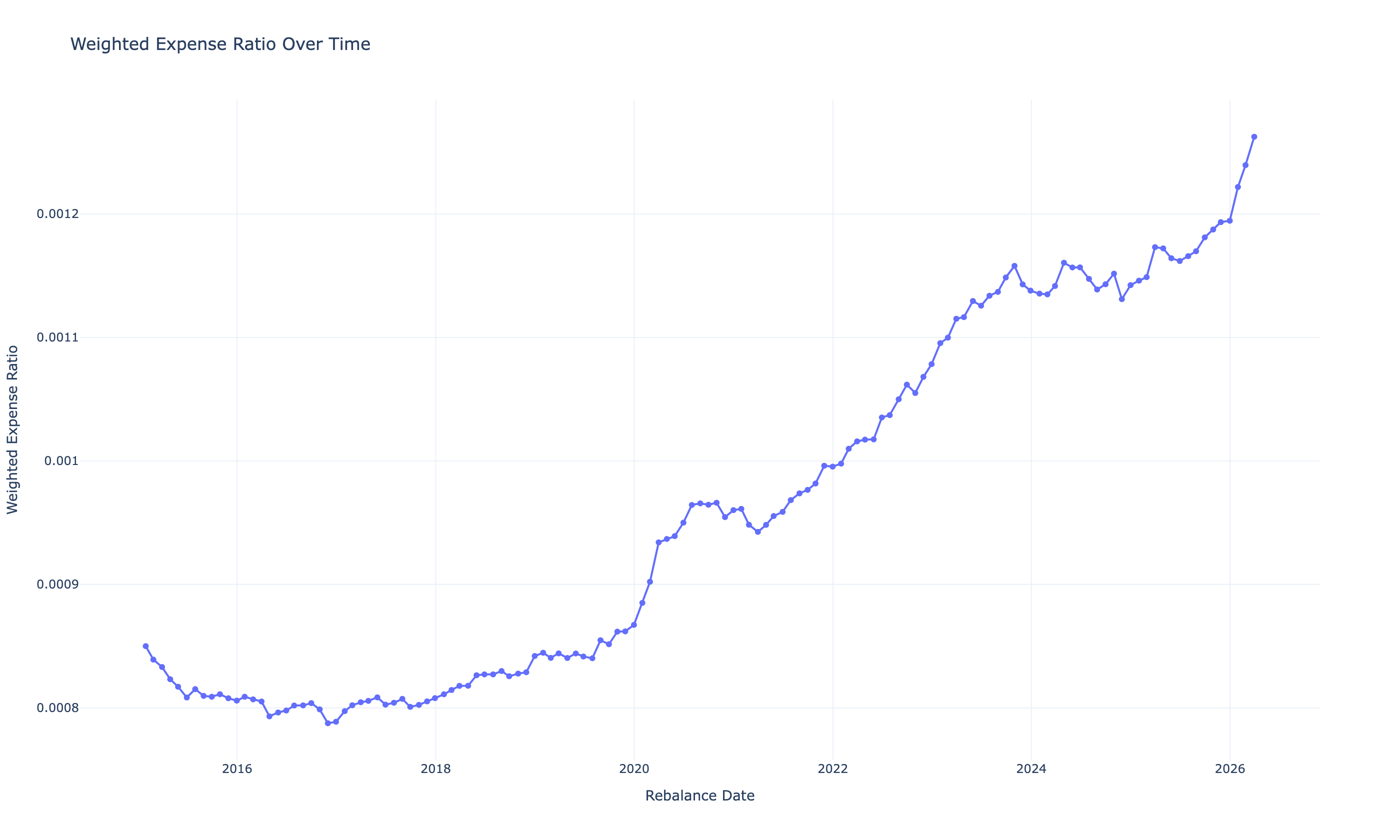

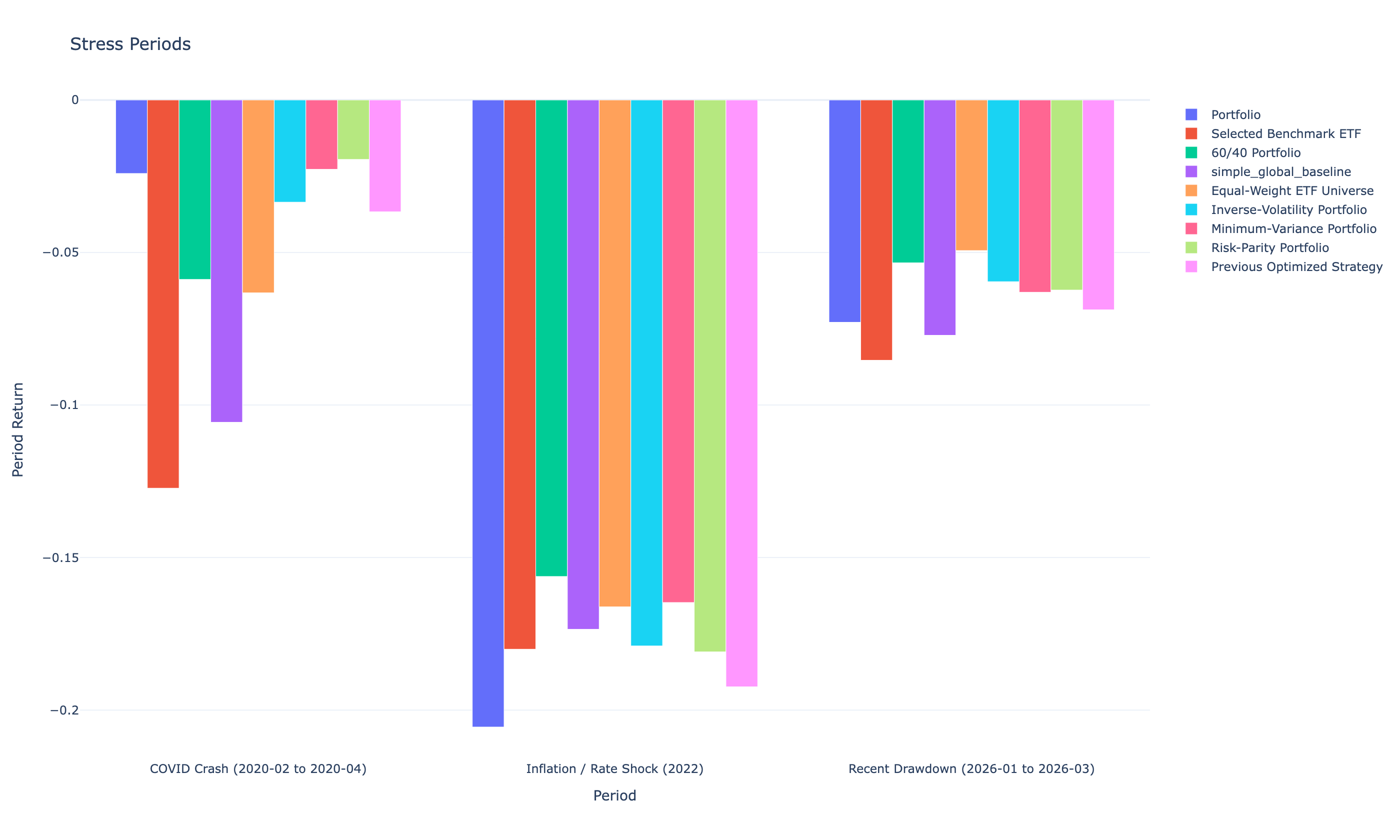

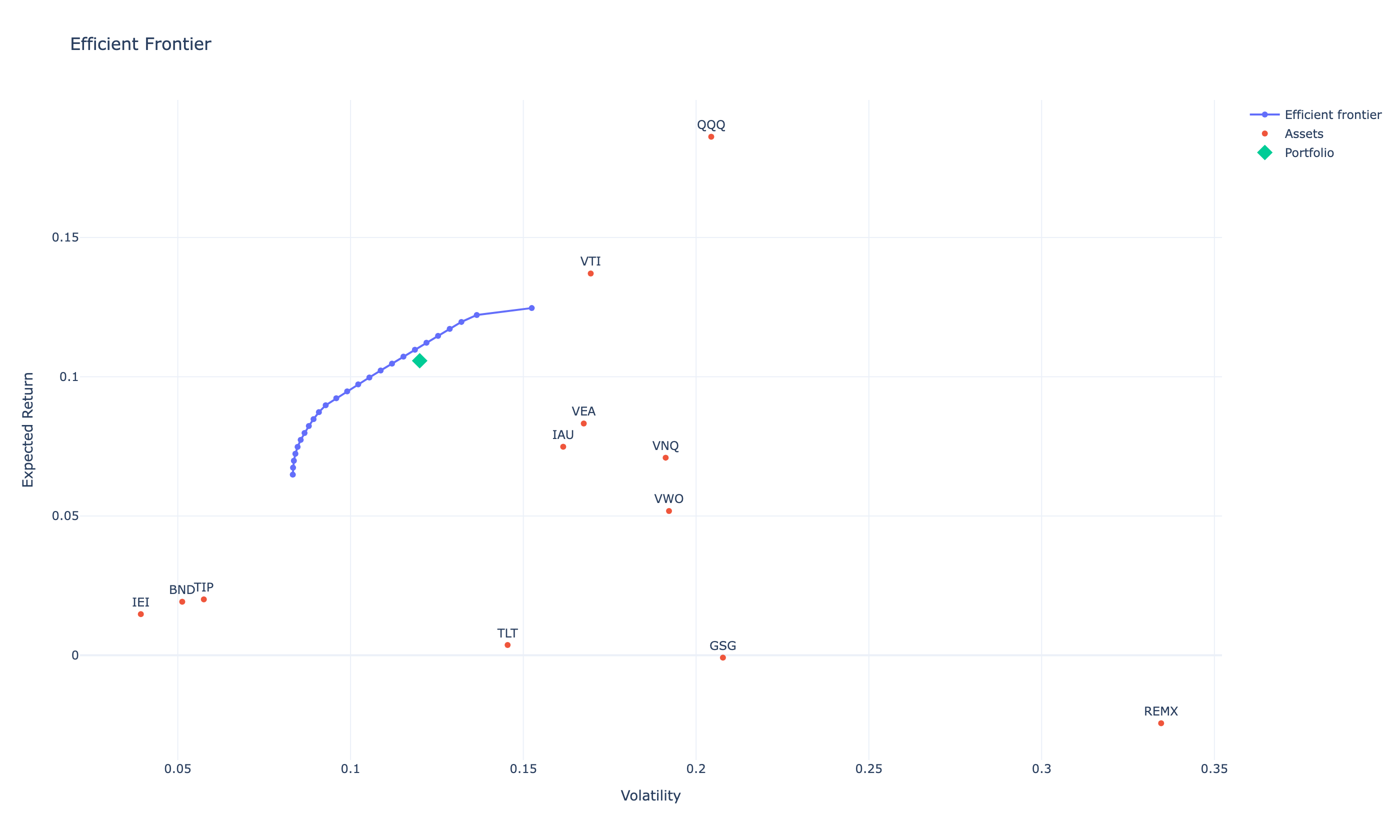

Charts

Twelve views of the same portfolio.

Take it with you

Downloads & provenance.

- Optimized portfolios — optimizer target weights and portfolio composition (.xlsx).

- Portfolio results — per-period backtest holdings and performance (.xlsx).

- Source repository ↗ — the pipeline, configs, and methodology docs that produced everything on this page.

Generated by run — from the committed report artifacts.